The American magazine business model is not one that depends heavily on single copy sales. It is a subscription based business model. No wonder than that some publishing companies seem disconnected from their newsstand departments despite the fact that sales at newsstand exceed 3 billion dollars and more than 100,000 stores sell magazines in the United States and Canada. Newsstand is a leading indicator of consumer trends but its complicated distribution system and financial terms such as RDA, IPO, rack fees, etc. make it difficult to embrace. In spite of its complexities, however, newsstand should be at the forefront of publishing because of its ability to predict future successes and failures for a publisher.

For example: Editors at a top-ranked, niche magazine radically adjusted editorial focus based upon two factors: a change in advertising strategy designed to expand sales opportunities, and recognition that the existing audience for the niche was contracting. The publisher’s marketing projection predicted a small decline in readership from core subscribers, but believed the gains from the new audience would outstrip the losses. The results, however, were far worse than the projections. The title successfully grew the new desired audience, but the success was mitigated by a rapid decline in existing audience. My team provided the disappointing results to consumer marketing, warning that similar declines might be recognized in renewals, and ultimately in direct mail results. Indeed, newsstand predicted the consumer marketing declines accurately and ultimately the title folded.

Samir Husni: COULD NEWSSTAND HAVE STOPPED THE DECLINE?

Luke Magerko: I can’t say, but the warning signs were clear. Many publishers do not think of newsstand as an early warning system, but I hope to change that. There are more than 100,000 stores selling magazines and, when analyzed, these stores tell a compelling story. My point is that newsstand can, and should be, the first stop in publishing analytics.

SH: WHY FOCUS ON PROFITABILITY?

LM: Profit provides the best context for decision making. For example, compare a weak analytic report (store count) versus a strong analytic report (store quality).

• Store Counts or “store quantity” are used as criteria for success in many newsstand departments. Simply, newsstand departments correlate store counts with vitality and directly correlate the number of stores to the title’s strength. The fallacy is that the store count implies all stores are equal. I am not making value judgments on the inherent quality of a store, but one average Walmart store has more sales impact than one convenience store. Therefore, giving equal weight to each store is misleading.

• I prefer to identify “quality stores.” A quality store is one that meets the profitability needs of a publisher. A title heavily reliant on achieving rate base will have a different definition of acceptable profit/loss than a niche special interest publication that has no rate base concern. Last week’s financial model meets both criteria.

A store-level profit/loss grid will determine correct store-level order regulation, and will lead to strategic marketing decisions. By summarizing store-level profitability into a chain profit/loss grid, publishers will quickly determine if a chain is worthy of checkout acquisition, promotion, or expansion into more stores.

SH: BUT ISN’T STORE QUANTITY AN ESSENTIAL TOOL TO DEMONSTRATE VITALITY AND AUDIENCE REACH?

LM: Store count is commonly used for just that purpose, but I disagree with that thinking. There are two weaknesses with the store count approach: replacement stores and stores with minimal draw (copies shipped). As mentioned earlier, if a publisher replaces one Walmart store with one convenience store, the store count report will show a net loss of zero, but sales will decline. I will go into more detail on the replacement stores in the future.

Let’s focus on one example of minimum draw: Current Draw of 1-2 per issue – Simply, I am analyzing a series of stores with a very low distribution, either one copy shipped to a store per issue or two copies shipped to a store per issue. I analyzed one top-200 ranked title who recently changed national distributors. One pretext for the switch was the promise of increased store counts. The chart (below) includes issue code, draw, and store count. As the draw declined, so too did the store count. The new national distributor assumed responsibility in May 2012. The October 2012 issue indicates the distributor achieved its promise by increasing store count while also reducing draw.

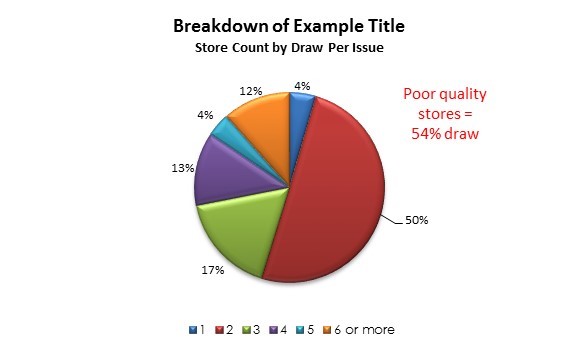

The pie chart (below) reflects the current draw by store. More than 50 percent of stores receive 1-2 copies per issue. Although the store count increased, the value of a 1-2 copies per store is weak. Here, overall sell through for the title is 24 percent, however the 1-2 copy stores sell at 14 percent sell through.

Overall, sales results from 1-2 copy stores are mixed: in a few instances (approximately 25 percent of the time), these low-draw stores perform on par with overall sell-through averages, but for the most part sales results remain underwhelming compared to the overall sell through.

SH: WHAT REPORTS ARE ESSENTIAL TO MAKING THE BEST DECISIONS?

LM: There are many reports essential to any newsstand tool kit. Four significant ones are: class of trade, region, county, and demographic (PRIZM Data). Some of these reports should be familiar, but they should be relied upon using the profitability model instead of as a plain sales report.

SH: HOW DO YOU USE CLASS OF TRADE REPORTING?

LM: The class of trade report is a standard newsstand report where one can quickly get a sense of a title’s market share in supermarkets, drug stores, etc. The deficiency with the class of trade report is that it is inherently skewed. Supermarkets represent approximately 35 percent of all magazine sales. Therefore if you are a top selling title, the class of trade report will reflect that supermarkets are the strongest category. If you are a smaller title, results are skewed to the bookstore class of trade which is the point of entry for smaller titles. Without profitability, the report provides no guidance on what to do next.

SH: WOULD THAT ALSO BE A CHALLENGE FOR REGIONAL REPORTING?

LM: Yes, regional reporting is another standard report that has little use in its current form. Some regional reports focus on four geographic regions, including the northeast, midwest, south, and west. Other regional reports break down regional reporting into sub regions. According to the United States Census Bureau, there are nine sub regions including:

• Northeast – New England

• Northeast – Mid-Atlantic

• South – South Atlantic

• South – East South Central

• South – West South Central

• Midwest – East North Central

• Midwest – West North Central

• Pacific – Mountain

• Pacific – Pacific Coast

Much like class of trade reporting, regional breakdowns are misleading because the three southern regions represent 37 percent of the population while the northeast represents 18 percent, the midwest represents 22 percent, and the west represents 23 percent. If the publisher analyzes a standard regional breakdown, most titles will have a strong market share in the south. This is a natural occurrence based on population trends, not a sales insight.

SH: HOW DOES YOUR PROFITABILITY MODEL HELP ENHANCE THESE REPORTS?

LM: Except for a handful of the largest titles which are fully penetrated into the 100,000-plus store universe, most titles have the potential for growth. Smaller titles certainly do not have full distribution into the full universe of stores currently selling magazines, but a profitability model will show how and where to expand distribution and to shape important editorial and marketing decisions. For example, if a title is consistently strong in the grocery class of trade and is strong in the northeast, the publisher should be encouraged to invest in display at Wegman’s. Conversely, poor showings in convenience stores recommend against promoting in those stores.

SH: CAN YOU PROVIDE AN EXAMPLE OF HOW THIS WORKS?

LM: Yes, unfortunately this is another negative example, however it makes the point. A mass-market publisher highlighted a sensitive cultural topic in a number of its issues. The issues were published a significant time ago, however the effect of the editorial choice lingers. Profitability within the areas that favor the cultural topic outperformed the unfavorable areas by a significant margin. The favorable regions generated 34 percent more profit per copy sold than their counterparts.

This input is a key insight because as checkout space or promotional opportunity presents itself, the publisher has a tool to aid in the decision-making process. Should the publisher promote in regions where sales are soft? Further, editorial staff and marketing groups have an important decision to make going forward on this topic – if and how to broach the same cultural issue on an ongoing basis.

SH: SO REGIONALITY DOES MATTER?

LM: My answer is a qualified yes. Politics and cultural issues have a lasting effect on regional magazine sales and profitability, however my sample size is fairly small to make a general proclamation. The good news is that by bringing together the full team of advertising, editorial, consumer marketing, and newsstand, the publishing group can make informed decisions based upon this powerful newsstand information. The effects can be identified, and a series of steps can be taken to mitigate negative effects.

SH: WHAT IS COUNTY REPORTING?

LM: County reporting is a far more accurate tool to gauge magazine audience than regional reporting. The United States is broken into four groups, A, B, C, and D, based upon the population of the county, A is largest and D is the smallest. County reporting reflects this sociological change by allowing analysts to look at urban, suburban, exurban, and rural makeup of an area to determine if there are sales patterns with these groups. Through technology, regional differences are becoming far less perceptible than in the past (with the exception of political and cultural issues) and county reporting helps reflect that. A.C. Nielsen defines the county breakdown as:

• “A County” is one of the top 25 counties by population in the United States (large urban)

• “B County” is one with a population of more than 150,000 that is not already an A County (inner suburbs).

• “C County” has between 40,000 and 150,000 residents (exurbs).

• “D County” is any other county (rural).

SH: ARE YOU SAYING THAT COUNTIES IN DIFFERENT PARTS OF THE COUNTRY ARE MORE SIMILAR THAN REGIONAL SIMILARITIES?

LM: Yes, I’ve found more sales correlation in the Upper East Side of Manhattan to the Lincoln Park district in Chicago than there are regional similarities between Chicago and Des Moines or New York City and Albany.

SH: DO YOU HAVE AN EXAMPLE OF HOW COUNTY DATA MIGHT BE BENEFICIAL?

LM: I have a case study to share: pricing based on county sales. I chose one of the most iconic brands in publishing, a top-40 title with a distinctive brand and an equally distinct audience. I applied the same conservative profitability estimates I discussed last week and determined this title is unprofitable at newsstand. This might be acceptable because the unit sales ensure rate base guarantees, however, there is a straightforward way for the publisher to enhance revenues.

I am generally not an advocate for price increases, but the data in this instance overwhelming. Looking at the chart (above), I analyzed three criteria by county. The urban “A” counties represent a plurality of stores, nearly a majority of sales, and are by far the least unprofitable group of stores. Without sharing the exact data, the price point is conducive to reach the C and D counties rather than targeting the known audience. This newsstand analysis should be used with the following criteria because newsstand results will mirror subscriber results:

• Who is the intended audience?

• What is the subscriber makeup for the title?

• Does it match newsstand?

• Where does the audience live?

SH: DOES NEWSSTAND SALES DATA REFLECT SUBSCRIBER DATA?

LM: There is a solid correlation between newsstand data and subscriber data, however more data points are necessary to concretely demonstrate the correlation. Again, my point is that newsstand data is the most rapid response system in the industry. I believe I read fifty-five percent of retail sales are recorded using point of sale data, according to the POS discussion at PBAA. It is imperative that this is data be integrated into reporting and used as the valuable tool it is because newsstand is a valuable conversation starter. That is, results seen at newsstand will predict an effect throughout the entire publishing house.

SH: WHAT IS PRIZM DATA?

LM: A.C. Nielsen provides an intriguing look at demography even deeper than county data by breaking counties down into smaller segments based on age, family size, and income. One national distributor provides that data as part of its service. Two specific reports can be generated using PRIZM data. Today I focus on income.

I analyzed a handful of titles using income and again found correlation between the subscriber and the stores where they shop. Using the zip code of a store, I estimated what kind of consumer is shopping in that store. This invaluable tool provides a deeper understanding of the customer.

Using the same iconic title described in the county data (see above), I demonstrated the need for a price increase by looking at both income levels and social attributes, essentially county breakdown by another name. The descriptions are self-explanatory, but please contact me at lmagerko@market-analytics.com for further detail. I color-coded the 5 most profitable groups in green, the middle 5 in yellow and the worst-performing groups in red. High income, urban consumers provide profitable sales while lower-income, rural consumers provide unprofitable sales. Again, my analysis sizes are too small to make sweeping statements, but Samir, as a man of the industry, may I ask this rhetorical question? If presented with an opportunity based on county data and PRIZM data, would this interest you?

SH: YES! SO THERE IS HOPE FOR GROWTH AFTER ALL!

LM: Yes! Our discussion last week focused on savings, not to discourage publishers, but to embolden them. I offered those tips as a precursor for this week’s look at potential opportunities.

I hope this week’s discussion inspires publishers to look inward and ask questions. I am thankful to have worked for progressive companies like Meredith and Diamond Comic Distributors which allowed me to test a great many hypothesis during my career. There are no bad hypotheses, but I feel our industry is so shell-shocked by declines that they have given up on growth. I say, start questioning and together we will grow this industry again!

Stay tuned. More to come. To read part one of this interview just see the blog entry below.